From the 1970s to Today: Home Prices vs. Incomes

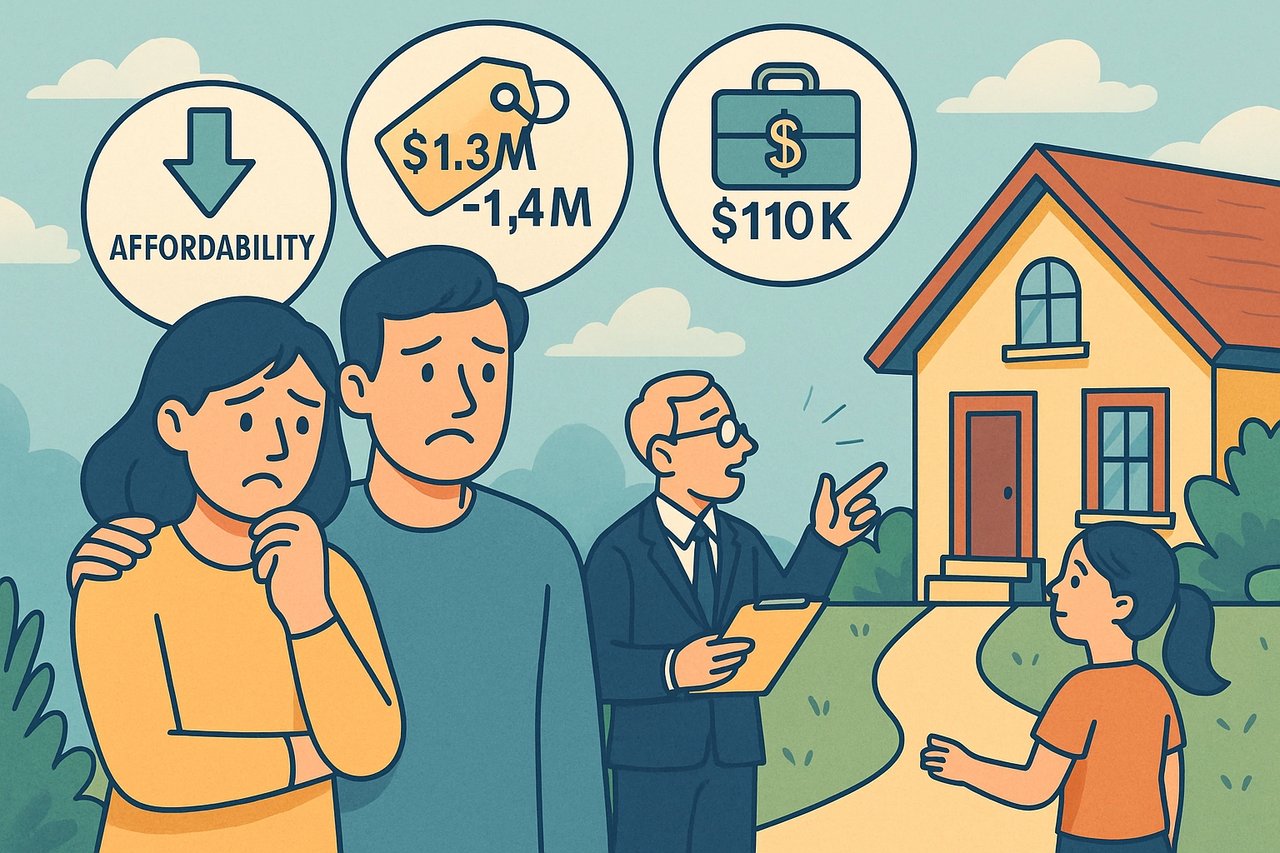

In the early 1970s, Orange County homes were remarkably affordable by today’s standards. For example, in 1970 a typical house sold for around $30,000 – roughly 3 times the median household income at the time. Fast forward to the present, and the median home price in Orange County is about $1.3 million, while the median household income is around $110,000. That’s a price‑to‑income ratio of nearly 12:1.

Even after adjusting for inflation, home values have soared far above what general cost‑of‑living increases can explain. To put it in perspective: Orange County’s median home price was ~$228,000 in 1990, and today it’s about $1.36 million – a roughly six‑fold increase. Meanwhile, median household incomes only doubled in that period (from roughly $55,000 in 2000 to $110,000 now). This widening gap means that where a previous generation might have bought a home on one income, today it might take two incomes and significant savings (or help from family) to achieve the same goal. It’s no wonder many parents worry whether their children will be able to afford a home here in Orange County.

Source: FHFA All‑Transactions House Price Index — Orange County & FRED Orange County Median Household Income.

Inflation, Dollar Devaluation & Monetary Policy

One major piece of the puzzle is macroeconomic forces – especially inflation and interest rates – which have dramatically shaped housing costs. In the late 1970s, the U.S. experienced high inflation, which drove up wages and prices across the board (including home prices). Then, to combat runaway inflation, the Federal Reserve pushed interest rates to record highs in the early 1980s. This had a chilling effect on housing: mortgage rates spiked above 16%–18% in 1981, which made loans extremely expensive and put homeownership out of reach for many. (Imagine a 30-year loan at 18% interest – it’s almost inconceivable to today’s buyers used to sub-7% rates!) Not surprisingly, home sales plummeted around 1981 and prices stagnated or fell in many areas in the early ’80s.

But in subsequent decades, the trend reversed. From the mid-1980s through 2021, interest rates saw a long-term decline, with occasional upticks. By 2000, mortgage rates were around 8%, and then after the 2008 financial crisis, the Federal Reserve slashed rates to historically low levels. In 2020–2021, we hit rock-bottom rates – the 30-year fixed averaged under 3% in 2021, the lowest on record. Cheap money enabled buyers to bid more for homes (since lower interest means lower monthly payments for the same loan amount). This fuelled rapid price appreciation. Indeed, there is a clear inverse relationship: as interest rates fell, home prices rose. After 2009, every dip in rates helped push home values higher. Between 2010 and 2021, Orange County home prices more than doubled (especially with the frenzy of 2020–2022 when rates were near 3%), far outpacing income growth.

Monetary policy played a direct role. The Federal Reserve not only set low short-term rates but also undertook massive bond-buying programs (Quantitative Easing) to pump money into the economy. The Fed bought trillions in mortgage-backed securities after 2008 and again in 2020, explicitly aiming to keep mortgage rates low and support the housing market. This flood of liquidity contributed to asset price inflation – meaning stocks, real estate, etc., all ballooned in value. As one analysis put it, “falling interest rates are a manifestation of monetary inflation, and monetary inflation often shows up as asset price inflation,” particularly housing. Essentially, the dollar’s value eroded (over 90% of its 1970 value is gone due to inflation), so tangible assets like houses became more expensive in dollar terms. A $30,000 house from 1970 might cost ~$200,000 today just from general inflation – but in OC it costs over $1 million, because extra factors magnified the increase.

Bottom line: ever since we left the gold standard in the early ’70s, the money supply has expanded dramatically, and each generation of buyers has faced higher nominal prices. Low interest rates made those prices temporarily affordable on a monthly basis, but when rates rise (as they did in 2022–2023 back to ~7%), the high principal costs turn into high payments too. Persistently low rates also encouraged investors to pour money into real estate for better returns, further driving up prices. The result is a classic inflationary spiral: more dollars chasing limited homes equals higher prices. One major piece of the puzzle is macroeconomic forces – especially inflation and interest rates – which have dramatically shaped housing costs... (up to “Not surprisingly” paragraph end). Source:

Rocket Mortgage: Historical 30‑Year Fixed‑Rate Mortgage Peaks (~16.6% in 1981).

Limited Supply, High Demand, and Local Market Dynamics

Macroeconomics aside, Orange County’s housing unaffordability is also a simple story of supply and demand in a very desirable area. Orange County grew rapidly in the late 20th century – its population jumped from ~700,000 in 1970 to over 3 million today. The region boasts excellent weather, job opportunities, and coastal amenities that attract people from across the country and world. However, building new housing here has not kept up with that demand. According to California’s Legislative Analyst’s Office, beginning in the 1970s, coastal counties built far fewer homes than needed, leading to a sustained shortage. Community resistance to development, strict zoning laws, environmental regulations (like 1970’s CEQA law), and the sheer lack of open land constrained new housing construction in Orange County. By the 1990s, OC was largely “built out” in the north and central areas, and South County’s master-planned communities filled in quickly. Source:

California Legislative Analyst’s Office – High Housing Costs Report.

When you have limited supply in a high-demand location, competition for homes becomes fierce. Buyers bid up prices – which is exactly what happened. By the 1980s, Orange County was regularly ranking as one of the least affordable markets. Only about 25% of OC households could afford the median-priced home in the late ’80s boom. And yet people kept coming, drawn by jobs and lifestyle, which sustained the pressure on prices. Every economic boom (late ’80s, early 2000s, late 2010s) saw OC home values surge to new heights, never really dropping back to their prior levels even after recessions.

Another local factor is trade-up demand and equity gains. Many long-time OC homeowners rode the wave of rising prices and accumulated significant home equity. When they sell, they have substantial wealth to reinvest or bid on another house, often outcompeting first-time buyers. Those who bought homes decades ago for $200k that are now worth $1M have a huge upper hand (and they’re not under pressure to sell unless they choose to). This dynamic means the housing stock in good school districts or coastal areas rarely “resets” to truly low prices – owners can wait out downturns. We saw this recently: after the 2008 crash, OC prices dipped around 30%, but then rebounded and hit new records by the mid-2010s. By late 2024, the median was about $1.2M (near an all-time high), despite the pandemic disruption and a rise in interest rates. Demand, buoyed by demographics and wealth, just keeps coming back.

Land values are a big part of the cost in Orange County. As a mostly built-out area, land is precious. Even a modest home in Costa Mesa or Mission Viejo now sits on land worth hundreds of thousands of dollars. This wasn’t the case in the 1970s when land was relatively cheap and plentiful. A builder in 1988 noted that in 1970, “I was selling houses here for $30k” but by the late ’80s “it’s $20,000 for the lot before you even start to build the house.” High development fees and infrastructure costs in California also add to new home prices. Thus, new construction tends to target the luxury end (to justify the costs), leaving fewer affordable starter homes being built.

Rental and investor trends play a role too. As buying became harder, more people rent longer, which pushes up rents and encourages investors to buy rental properties, further reducing entry-level inventory. Orange County also sees buyers from overseas or other parts of California investing here, given its stability and prestige, which can drive prices beyond what local salaries alone would support.

Lastly, consider policy changes like Proposition 13 (1978), which capped property tax increases. Prop 13 made it easier for longtime owners to hold homes (low taxes even as values soared), but it also meant local governments had less incentive to approve housing (since new development doesn’t hugely boost tax revenue). Some argue this contributed to the slow housing growth in California. Additionally, the mortgage interest deduction and other policies have historically incentivized buying, which increases demand (though those benefits mainly help higher earners).

In summary, Orange County’s housing became a hot commodity: too many people chasing too few homes. Economics 101 says that drives prices up – and indeed, by 2025 Orange County leads the nation in housing costs, with even neighboring L.A. County lagging behind (LA’s median is around $900k while OC’s is $1.4M+). It’s a perfect storm of desirability, limited supply, and wealth in the market.

The Changing Mortgage and Lending Landscape

Another piece of the affordability story is how buying a home itself changed between our parents’ generation and today. In the 1970s, a typical buyer might put 20% down and take a straightforward 30-year fixed mortgage. There were no gimmicky loans, and banks applied strict income-to-payment ratios. This conservative financing kept prices in check to some degree: you couldn’t pay more for a house unless you saved more or earned more, period.

Starting in the 1990s and especially the early 2000s, the lending environment loosened. Banks and new mortgage companies introduced low down payment programs, interest-only loans, and even zero-down or subprime loans by the mid-2000s. This culminated in the housing bubble of 2004–2006, where virtually anyone could get a loan, and many buyers stretched to afford homes with little money down. The easy credit temporarily increased affordability in terms of getting into a home, but it also inflated prices—lots of new buyers entered the market, bidding up values on risky financing. We all know how that ended: the 2008 crash led to a wave of foreclosures and a sharp but short-lived drop in home prices.

Post-2008, lending standards tightened again—no more “no-doc” ninja loans; borrowers had to fully document income and meet ability-to-repay rules. This has kept today’s market more stable, but it also means no quick fixes for affordability through creative loans. If anything, strict lending coupled with high prices means many first-time buyers simply can’t qualify for the mortgage needed. One silver lining: those who do buy are less likely to default now, and downturns haven’t seen mass foreclosures driving prices down—but that also means we haven’t seen big price corrections to make homes cheaper.

Another change: length of homeownership tenure has increased. People are staying in their homes longer (the average length is now 12+ years, up from ~6 years in 2005). Fewer homes on the resale market each year contributes to scarcity, especially of affordable starter homes. Many Baby Boomers are aging in place rather than downsizing, and some who do sell are helping their kids buy homes (intergenerational assistance), which again doesn’t increase overall supply.

Finally, it’s worth mentioning interest rate volatility in recent years. In 2022, the Fed aggressively raised rates to fight inflation, pushing mortgage rates from ~3% to ~7% in a matter of months. This sudden spike in rates was like slamming the brakes—it reduced buyers’ purchasing power by 30%+ overnight. Normally, that would cause home prices to fall significantly. In Orange County, we did see the frenzy cool in 2023, but prices remained high (sellers were reluctant to drop prices, and many would-be sellers just stayed put with their low-interest mortgages). The market here turned very sluggish rather than crashing—affordability hit record lows as a result, because now you needed both a high price and to afford a 7% interest payment. Mortgage payments as a share of income reached some of their highest levels in decades in 2023, even though prices only dipped slightly, due to those higher rates. Essentially, today’s buyers face the worst of both worlds: high home values and higher interest, a combination that makes monthly payments punishingly expensive for first-timers.

The lending and policy landscape, in short, has oscillated between periods of easy money (which drove prices up) and periods of tight money (which made buying difficult but didn’t fully reverse the price gains). Through it all, Orange County housing has ratcheted upward, each cycle lifting the “floor” of prices higher.

Source:

Bankrate: Historical Mortgage Rates.

Finding Hope: Strategies for Today’s Parents and First-Time Buyers

Reading about all these challenges can feel overwhelming—we get it. As local real estate professionals and parents ourselves, we have seen the struggles and anxieties firsthand. While there’s no magic wand to bring OC home prices back to 1970s levels, there are strategies and resources that can help families make homeownership more attainable.

One rising trend is co-buying or multi-generational living. By pooling resources, co-buyers can afford more house or qualify for a loan they couldn’t get alone. Nearly 15% of Americans have co-purchased a home with someone other than a spouse, and almost half of young adults say they’d consider it. It might be siblings teaming up, or parents and adult children buying a property together. Similarly, multi-generational households—young families moving in with parents, or vice versa—have become more common, often to save money. These arrangements can be win-win: sharing a home means sharing expenses, and it allows time to build equity. If you go this route, be sure to spell out agreements upfront so everyone’s interests are protected.

Don’t assume you’re on your own when it comes to that hefty down payment. There are programs at the state, local, and even employer level to help. For example, California’s “Dream For All” program was launched to provide up to 20% down payment assistance to first-time, first-generation buyers. In its initial round in 2023, thousands benefitted (the funds were so popular the program is now moving to a lottery system). With these shared-appreciation loans, the state fronts your down payment, and you repay a portion of the home’s appreciation when you sell. There are also traditional down payment assistance loans and grants (often for moderate-income buyers) through CalHFA and other agencies. It’s worth exploring these if saving 20% (or even 5%) feels impossible.

Beyond conventional buying, consider alternative paths such as buying a townhome or condo as a starter, which is often significantly cheaper than a detached house. You can build equity in a condo and later trade up. Look into new home communities farther inland, or even in the Inland Empire, where prices are lower and incentives may be available. Some families choose to relocate to a less expensive area to buy a home, with a plan to potentially return to OC later. Also, Accessory Dwelling Units (ADUs) or duplex homes can help: you live in one part and rent out the other to help pay the mortgage.

For parents hoping to help their kids, or first-time buyers with generous relatives, early inheritance and family assistance can bridge the gap. Many parents and grandparents in OC are tapping their home equity or savings to give children a leg up on the down payment (often as a gift or interest-free loan). Even $10,000 or $20,000 gifted can make a difference in qualifying for a mortgage or avoiding PMI. Multi-generational wealth building is a long game: by helping the next generation buy in now, families can keep that California Dream alive. If you’re a homeowner, it’s also wise to engage in estate planning to help your kids avoid tax shocks if they inherit your home.

Lastly, whether you plan to buy now or five years from now, get educated and prepared. Improve your credit score (higher scores can significantly lower your interest rate offered). Reduce other debts if possible. Run the numbers with a reputable lender or use a home affordability calculator to see what price range is feasible and what savings you’ll need. Sometimes the results are pleasantly surprising; other times they provide a concrete savings target. If you find you’re still priced out, don’t be discouraged—the market evolves, and with diligent planning (and maybe some of the strategies above), doors can open.

Above all, stay encouraged. It’s easy to feel defeated reading headlines about high prices, but ownership is not out of reach if you take it step by step and utilize the resources available. Many buyers are finding success through creative means and prudent planning. And every year, new programs or opportunities can emerge.

Source:

California Dream For All Down Payment Program.

Conclusion: The Orange County Dream, Reimagined

Housing in Orange County has become dramatically more expensive since the 1970s – there’s no sugarcoating that. The combination of inflation, limited supply, favorable climate, and economic growth turned OC real estate into a high-priced commodity. However, while the rules of the game have changed, the dream of homeownership is not dead. It may require a new mindset (perhaps buying a condo instead of a house, or partnering with family, or considering areas you hadn’t before) and leveraging every tool in the toolkit (assistance programs, creative financing, etc.), but it’s still achievable.

For parents anxious about their kids’ future, there is hope in knowledge and preparation. Open conversations about money and realistic goals are a great start. For first-time buyers feeling discouraged, know that you’re not alone – many others are in the same boat, and a community of professionals and programs exists to help you. The path to owning a home in Orange County might be longer now than it was decades ago, but with persistence, smart strategies, and maybe a bit of help, you can get there.

If you’d like personalized guidance on navigating Orange County’s market, our team at Verso Homes is here to help with warmth and expertise. We’ve helped families strategize everything from co-buying agreements to leveraging equity from a previous home, and we stay up-to-date on the latest programs to assist buyers. The road may be challenging, but with the right plan and support, you or your children will have a place to call home in this beautiful community.

Ready to explore your options or need advice tailored to your situation?

Contact Verso Homes for a friendly chat. We’re not just realtors, we’re neighbors who understand the journey. Let’s work together to make the Orange County dream a reality for your family.

Empathy and expertise are powerful allies – and you have more of both on your side than you may think. Happy home hunting!

*Market data may change. Please verify information with your real estate advisor or lender.